Walkthrough for the CLVTools Package

Patrick Bachmann

Patrik Schilter

Jeffrey Näf

Markus Meierer

September 15, 2024

Source:vignettes/CLVTools.Rmd

CLVTools.RmdAbstract

This vignette is a hands-on guide to the R package

CLVTools for modeling and forecasting customer base

dynamics. It shows how to construct clv.data objects,

estimate latent attrition models (Pareto/NBD, BG/NBD, GGom/NBD),

and generate individual-level forecasts: conditional expected

transactions (CET), probability of being alive (PAlive), and

discounted expected residual (or finite-horizon) transactions

(DERT/DECT). We demonstrate the use of time-invariant and

time-varying covariates, optional purchase–attrition correlation

via a Sarmanov specification, and regularization and equality

constraints for covariate effects. The vignette also covers the

Gamma/Gamma spending model for predicting mean spend and computing

CLV, and provides reproducible code for summaries, diagnostics,

and plots. Guidance on data preparation, estimation/holdout

splitting, optimizer settings, and result interpretation is

included throughout.

Prerequisites: Setup the R environment

Install the stable version from CRAN:

install.packages("CLVTools")Install the development version from GitHub (using the

devtools package (Wickham, Hester,

and Chang 2019)):

install.packages("devtools")

devtools::install_github("bachmannpatrick/CLVTools", ref = "development")Load the package

Apply the CLVTools Package

General workflow

Independent of the latent attrition model applied in

CLVTools, the general workflow consists of three main

steps:

Create a

clv.dataobject containing the dataset and required meta-information such as date formats and column names in the dataset. After initializing the object, there is the option to add additional information on covariates in a separate step.Fit the model on the data provided.

Use the estimated model parameters to predict future customer purchase behavior.

CLVTools

CLVTools provides two ways for evaluating latent

attrition models: you can use of the provided formula interface or you

can use standard functions (non-formula interface). Both offer the same

functionality, however the formula interface is especially helpful when

covariates are included in the model. Through out this walkthrough, we

will illustrate both options.

Reporting and plotting results is facilitated by the implementation

of well-known generic methods such as plot(),

print() and summary(). These commands adapt

their output according to the model state and may be used at any point

of the workflow.

Load sample data provided in the package

As Input data CLVTools requires customers’ transaction

history. Every transaction record consists of a purchase date and

customer ID. Optionally, the price of the transaction may be included to

allow for prediction of future customer spending using an additional

Gamma/Gamma model(Fader, Hardie, and Lee 2005b;

Colombo and Jiang 1999). Using the full history of transaction

data allows for comprehensive plots and summary statistics, which allow

the identification of possible issues prior to model estimation. Data

may be provided as data.frame or data.table

(Dowle and Srinivasan 2019).

It is common practice to split time series data into two parts, an estimation and a holdout period. The model is estimated based on the data from the estimation period while the data from the holdout period allows to rigorously assess model performance. Once model performance is checked on known data one can proceed to predict data without a holdout period. The length of the estimation period is heavily dependent on the characteristics of the analyzed dataset. We recommend to choose an estimation period that contains in minimum the length of the average inter-purchase time. Note that all customers in the dataset need to purchase at least once during the estimation period, i.e. these models do not account for prospects who have not yet a purchase record.

Some models included in CLVTools allow to model the

impact of covariates. These covariates may explain heterogeneity among

the customers and therefore increase the predictive accuracy of the

model. At the same time, we may also identify and quantify the effects

of these covariates on customer purchase and customer attrition.

CLVTools distinguishes between time-invariant and

time-varying covariates. Time-invariant covariates include customer

characteristics such as demographics that do not change over time.

Time-varying covariates are allowed to change over time. They include

for example direct marketing information or seasonal patterns.

For the following example, we use simulated data comparable to data

from a retailer in the apparel industry. The dataset contains

transactional detail records for every customer consisting of customer

id, date of purchase and the total monetary value of the transaction.

The apparel dataset is available in the CLVTools package.

Use the data(apparelTrans) to load it:

data("apparelTrans")

apparelTrans

#> Id Date Price

#> <char> <Date> <num>

#> 1: 1 2005-01-02 230.30

#> 2: 1 2005-09-06 84.39

#> 3: 1 2006-01-18 131.07

#> 4: 1 2006-04-05 86.43

#> 5: 1 2006-07-02 11.49

#> ---

#> 3183: 600 2005-01-02 24.94

#> 3184: 600 2005-04-17 54.97

#> 3185: 600 2005-06-30 66.84

#> 3186: 600 2005-10-27 22.54

#> 3187: 600 2006-01-09 12.97Initialize the CLV-Object

Before we estimate a model, we are required to initialize a data

object using the clvdata() command. The data object

contains the prepared transactional data and is later used as input for

model fitting. Make sure to store the generated object in a variable,

e.g. in our example clv.apparel.

Be aware that probabilistic models such as the ones implemented in

CLVTools are usually applied to specific customer cohorts.

That means, you analyze customer that have joined your company at the

same time (usually same day, week, month, or quarter). For more

information on cohort analysis, see also here.

Consequently, the data apparelTrans in this example is not the full

transaction records of a fashion retailer, but rather only the customer

cohort of 250 customers purchasing for the first time at this business

on the day of 2005-01-03. This has to be done before initializing a data

object using the clvdata() command.

Through the argument data.transactions a

data.frame or data.table which contains the

transaction records, is specified. In our example this is

data.transactions=apparelTrans. The argument

date.format is used to indicate the format of the date

variable in the data used. The date format in the apparel dataset is

given as “year-month-day” (i.e., “2005-01-03”), therefore we set

date.format="ymd". Other combinations such as

date.format="dmy" are possible. See the documentation of

lubridate (Grolemund and Wickham

2011) for all details. time.unit is the scale used

to measure time between two dates. For this dataset and in most other

cases The argument time.unit="week" is the preferred

choice. Abbreviations may be used (i.e. “w”).

estimation.split indicates the length of the estimation

period. Either the length of the estimation period (in previous

specified time units) or the date at which the estimation period ends

can be specified. If no value is provided, the whole dataset is used as

estimation period (i.e. no holdout period). In this example, we use an

estimation period of 40 weeks. Finally, the three name arguments

indicate the column names for customer ID, date and price in the

supplied dataset. Note that the price column is optional.

clv.apparel <- clvdata(apparelTrans,

date.format="ymd",

time.unit = "week",

estimation.split = 104,

name.id = "Id",

name.date = "Date",

name.price = "Price")Check the clvdata Object

To get details on the clvdata object, print it to the

console.

clv.apparel

#> CLV Transaction Data

#>

#> Call:

#> clvdata(data.transactions = apparelTrans, date.format = "ymd",

#> time.unit = "week", estimation.split = 104, name.id = "Id",

#> name.date = "Date", name.price = "Price")

#>

#> Total # customers 600

#> Total # transactions 3183

#> Spending information TRUE

#>

#>

#> Time unit Weeks

#>

#> Estimation start 2005-01-02

#> Estimation end 2006-12-31

#> Estimation length 104.0000 Weeks

#>

#> Holdout start 2007-01-01

#> Holdout end 2010-12-20

#> Holdout length 207.0000 WeeksAlternatively the summary() command provides full

detailed summary statistics for the provided transactional detail.

summary() is available at any step in the process of

estimating a probabilistic customer attrition model with

CLVTools. The result output is updated accordingly and

additional information is added to the summary

statistics.nobs() extracts the number of observations. For

the this particular dataset we observe a total of 250 customers who made

in total 2257 repeat purchases. Approximately 26% of the customers are

zero repeaters, which means that the only a minority of the customers do

not return to the store after their first purchase.

summary(clv.apparel)

#> CLV Transaction Data

#>

#> Time unit Weeks

#> Estimation length 104.0000 Weeks

#> Holdout length 207.0000 Weeks

#>

#> Transaction Data Summary

#> Estimation Holdout Total

#> Period Start 2005-01-02 2007-01-01 2005-01-02

#> Period End 2006-12-31 2010-12-20 2010-12-20

#> Number of customers - - 600

#> First Transaction in period 2005-01-02 2007-01-01 2005-01-02

#> Last Transaction in period 2006-12-31 2010-12-20 2010-12-20

#> Total # Transactions 1866 1317 3183

#> Mean # Transactions per cust 3.110 5.557 5.305

#> (SD) 2.714 5.123 6.119

#> Mean Spending per Transaction 40.545 36.977 39.069

#> (SD) 73.362 55.356 66.519

#> Total Spending 75657.730 48699.170 124356.900

#> Total # zero repeaters 213 - -

#> Percentage of zero repeaters 35.500 - -

#> Mean Interpurchase time 24.823 30.604 37.817

#> (SD) 19.417 24.756 42.339Estimate Model Parameters

After initializing the object, we can start estimating the first

probabilistic latent attrition model. We start with the standard

Pareto/NBD model (Schmittlein, Morrison, and

Colombo 1987) and therefore use the command pnbd()

to fit the model and estimate model parameters. clv.data

specifies the initialized object prepared in the last step. Optionally,

starting values for the model parameters and control settings for the

optimization algorithm may be provided: The argument

start.params.model allows to assign a vector

(e.g. c(alpha=1, beta=2, s=1, beta=2) in the case of the

Pareto/NBD model) of starting values for the optimization. This is

useful if prior knowledge on the parameters of the distributions are

available. By default starting values are set to 1 for all parameters.

The argument optimx.args provides an option to control

settings for the optimization routine. It passes a list of arguments to

the optimizer. All options known from the package optimx

(Nash and Varadhan 2011; Nash 2014) may be

used. This option enables users to specify specific optimization

algorithms, set upper and/or lower limits or enable tracing information

on the progress of the optimization. In the case of the standard

Pareto/NBD model, CLVTools uses by default the optimization

method L-BFGS-G (Byrd et al.

1995). If the result of the optimization is in-feasible, the

optimization automatically switches to the more robust but often slower

Nelder-Mead method (Nelder and Mead

1965). verbose shows additional output.

To execute the model estimation you have the choice between a formula-based interface and a non-formula-based interface. In the following we illustrate the two alternatives.

Estimating the model using formula interface:

est.pnbd <- latentAttrition(formula = , family = pnbd, data=clv.apparel)

#> Starting estimation...

#> Estimation finished!

est.pnbd

#> Pareto/NBD Standard Model

#>

#> Call:

#> latentAttrition(family = pnbd, data = clv.apparel)

#>

#> Coefficients:

#> r alpha s beta

#> 1.4490 48.6361 0.5613 46.8844

#> KKT1: TRUE

#> KKT2: TRUE

#>

#> Used Options:

#> Correlation: FALSEUsing start parameters and other additional arguments for the optimzier:

est.pnbd <- latentAttrition(formula = , family = pnbd, data=clv.apparel,

optimx.args = list(control=list(trace=5),

method="Nelder-Mead"),

start.params.model=c(r=1, alpha=10, s=2, beta=8))Estimating the model using non-formula interface:

est.pnbd <- pnbd(clv.data = clv.apparel)

est.pnbdIf we assign starting parameters and additional arguments for the optimizer we use:

est.pnbd <- pnbd(clv.data = clv.apparel,

start.params.model = c(r=1, alpha = 2, s = 1, beta = 2),

optimx.args = list(control=list(trace=5),

method="Nelder-Mead"

))Parameter estimates may be reported by either printing the estimated

object (i.e. est.pnbd) directly in the console or by

calling summary(est.pnbd) to get a more detailed report

including the likelihood value as well as AIC and BIC. Alternatively

parameters may be directly extracted using coef(est.pnbd).

Also loglik(), confint() and

vcov() are available to directly access the Loglikelihood

value, confidence intervals for the parameters and to calculate the

Variance-Covariance Matrix for the fitted model. For the standard

Pareto/NBD model, we get 4 parameters

and

.

where

represent the shape and scale parameter of the gamma distribution that

determines the purchase rate and

of the attrition rate across individual customers.

can be interpreted as the mean purchase and

as the mean attrition rate. Note that the significance indicators are

set to NA for each parameter. The main model parameters are

by definition always strictly positive and a hypothesis test relative to

a null of 0 therefore does not make sense. In the case of the

apparelTrans dataset we observe a an average purchase rate of

transactions and an average attrition rate of

per customer per week. KKT 1 and 2 indicate the Karush-Kuhn-Tucker

optimality conditions of the first and second order (Kuhn and Tucker 1951). If those criteria are

not met, the optimizer has probably not arrived at an optimal solution.

If this is the case it is usually a good idea to rerun the estimation

using alternative starting values.

#Full detailed summary of the parameter estimates

summary(est.pnbd)

#> Pareto/NBD Standard Model

#>

#> Call:

#> latentAttrition(family = pnbd, data = clv.apparel)

#>

#> Fitting period:

#> Estimation start 2005-01-02

#> Estimation end 2006-12-31

#> Estimation length 104.0000 Weeks

#>

#> Coefficients:

#> Estimate Std. Error z-val Pr(>|z|)

#> r 1.4490 0.2434 NA NA

#> alpha 48.6361 7.4892 NA NA

#> s 0.5613 0.2710 NA NA

#> beta 46.8844 35.6114 NA NA

#>

#> Optimization info:

#> LL -5848.0978

#> AIC 11704.1957

#> BIC 11721.7834

#> KKT 1 TRUE

#> KKT 2 TRUE

#> fevals 25.0000

#> Method L-BFGS-B

#>

#> Used Options:

#> Correlation FALSE

#Extract the coefficients only

coef(est.pnbd)

#> r alpha s beta

#> 1.4489768 48.6360845 0.5612598 46.8843633

#Alternative: oefficients(est.pnbd.obj)To extract only the coefficients, we can use coef(). To

access the confidence intervals for all parameters

confint() is available.

#Extract the coefficients only

coef(est.pnbd)

#> r alpha s beta

#> 1.4489768 48.6360845 0.5612598 46.8843633

#Alternative: oefficients(est.pnbd.obj)

#Extract the confidence intervals

confint(est.pnbd)

#> 2.5 % 97.5 %

#> r 0.97186638 1.926087

#> alpha 33.95755823 63.314611

#> s 0.03001563 1.092504

#> beta -22.91272141 116.681448In order to get the Likelihood value and the corresponding Variance-Covariance Matrix we use the following commands:

# LogLikelihood at maximum

logLik(est.pnbd)

#> 'log Lik.' -5848.098 (df=4)

# Variance-Covariance Matrix at maximum

vcov(est.pnbd)

#> r alpha s beta

#> r 0.05925727 1.7049763 -0.01786467 -3.472617

#> alpha 1.70497627 56.0878417 -0.43375973 -82.963758

#> s -0.01786467 -0.4337597 0.07346698 9.366245

#> beta -3.47261652 -82.9637580 9.36624544 1268.172657As an alternative to the Pareto/NBD model CLVTools

features the BG/NBD model (Fader, Hardie, and Lee

2005a) and the GGomp/NBD (Bemmaor and

Glady 2012). To use the alternative models replace

pnbd() by the corresponding model-command. Note that he

naming and number of model parameters is dependent on the model. Consult

the manual for more details on the individual models. Beside

probabilistic latent attrition models, CLVTools also

features the Gamma/Gamma model (Colombo and Jiang

1999; Fader, Hardie, and Lee 2005a) which is used to predict

customer spending. See section Customer Spending

for details on the spending model.

| Command | Model | Covariates | Type | |

|---|---|---|---|---|

| pnbd() | Pareto/NBD | time-invariant & time-varying | latent attrition model | |

| bgnbd() | BG/NBD | time-invariant | latent attrition model | |

| ggomnbd() | GGom/NBD | time-invariant | latent attrition model | |

| gg() | Gamma/Gamma | - | spending model |

To estimate the GGom/NBD model we apply the ggomnbd()to

the clv.apparel object. The GGom/NBD model is more flexible

than the Pareto/NBD model, however it sometimes is challenging to

optimize. Note that in this particular case providing start parameters

is essential to arrive at an optimal solution

(i.e. kkt1: TRUE and kkt2: TRUE).

To execute the model estimation you have the choice between a formula-based interface and a non-formula-based interface. In the following we illustrate the two alternatives.

Estimating the model using formula interface:

est.ggomnbd <- latentAttrition(formula = , family = ggomnbd, data=clv.apparel,

optimx.args = list(method="Nelder-Mead"),

start.params.model=c(r=0.7, alpha=5, b=0.005, s=0.02, beta=0.001))Predict Customer Behavior

Once the model parameters are estimated, we are able to predict

future customer behavior on an individual level. To do so, we use

predict() on the object with the estimated parameters

(i.e. est.pnbd). The prediction period may be varied by

specifying prediction.end. It is possible to provide either

an end-date or a duration using the same time unit as specified when

initializing the object (i.e prediction.end = "2006-05-08"

or prediction.end = 30). By default, the prediction is made

until the end of the dataset specified in the clvdata()

command. The argument continuous.discount.factor allows to

adjust the discount rate used to estimated the discounted expected

transactions (DERT). The default value is 0.1 (=10%). Make

sure to convert your discount rate if you use annual/monthly/weekly

discount rates. An annual rate of (100 x d)\% equals a

continuous rate delta = ln(1+d). To account for time units

which are not annual, the continuous rate has to be further adjusted to

delta=ln(1+d)/k, where k are the number of

time units in a year. Probabilistic customer attrition model predict in

general three expected characteristics for every customer:

- “conditional expected transactions” (CET), which is the number of transactions to expect form a customer during the prediction period,

- “probability of a customer being alive” (PAlive) at the end of the estimation period and

- “discounted expected residual transactions” (DERT) for every customer, which is the total number of transactions for the residual lifetime of a customer discounted to the end of the estimation period.

If spending information was provided when initializing the

clvdata-object, CLVTools provides prediction

for

- predicted mean spending estimated by a Gamma/Gamma model (Colombo and Jiang 1999; Fader, Hardie, and Lee 2005a) and

- the customer lifetime value (CLV). CLV is calculated as the product of DERT and predicted spending.

If a holdout period is available additionally the true numbers of transactions (“actual.x”) and true spending (“actual.period.spending”) during the holdout period are reported.

To use the parameter estimates on new data (e.g., an other customer

cohort), the argument newdata optionally allows to provide

a new clvdata object.

results <- predict(est.pnbd)

#> Predicting from 2007-01-01 until (incl.) 2010-12-20 (207.14 Weeks).

#> Estimating gg model to predict spending...

#> Starting estimation...

#> Estimation finished!

print(results)

#> Key: <Id>

#> Id period.first period.last period.length actual.x

#> <char> <Date> <Date> <num> <int>

#> 1: 1 2007-01-01 2010-12-20 207.1429 0

#> 2: 10 2007-01-01 2010-12-20 207.1429 1

#> 3: 100 2007-01-01 2010-12-20 207.1429 9

#> 4: 101 2007-01-01 2010-12-20 207.1429 0

#> 5: 102 2007-01-01 2010-12-20 207.1429 0

#> ---

#> 596: 95 2007-01-01 2010-12-20 207.1429 4

#> 597: 96 2007-01-01 2010-12-20 207.1429 3

#> 598: 97 2007-01-01 2010-12-20 207.1429 0

#> 599: 98 2007-01-01 2010-12-20 207.1429 0

#> 600: 99 2007-01-01 2010-12-20 207.1429 0

#> actual.period.spending PAlive CET DERT

#> <num> <num> <num> <num>

#> 1: 0.00 0.9468478 7.3256573 0.46765602

#> 2: 14.37 0.9825606 3.5198114 0.22469806

#> 3: 333.35 0.2784686 0.4190901 0.02675392

#> 4: 0.00 0.4739762 1.2056215 0.07696458

#> 5: 0.00 0.2784686 0.4190901 0.02675392

#> ---

#> 596: 98.81 0.8978209 3.2162499 0.20531927

#> 597: 253.61 0.2784686 0.4190901 0.02675392

#> 598: 0.00 0.2784686 0.4190901 0.02675392

#> 599: 0.00 0.6024098 1.5323094 0.09781972

#> 600: 0.00 0.9416701 4.3513967 0.27778489

#> predicted.mean.spending predicted.period.spending predicted.CLV

#> <num> <num> <num>

#> 1: 88.64634 649.39268 41.455992

#> 2: 41.21027 145.05238 9.259868

#> 3: 37.62791 15.76949 1.006694

#> 4: 34.56278 41.66962 2.660110

#> 5: 37.62791 15.76949 1.006694

#> ---

#> 596: 26.54863 85.38701 5.450944

#> 597: 37.62791 15.76949 1.006694

#> 598: 37.62791 15.76949 1.006694

#> 599: 35.83393 54.90868 3.505265

#> 600: 19.20941 83.58774 5.336082To change the duration of the prediction time, we use the

predicton.end argument. We can either provide a time period

(30 weeks in this example):

predict(est.pnbd, prediction.end = 30)or provide a date indication the end of the prediction period:

predict(est.pnbd, prediction.end = "2006-05-08")Plotting

CLVTools, offers a variety of different plots. All

clvdata objects may be plotted using the

plot() command. Similar to summary(), the

output of plot() and the corresponding options are

dependent on the current modeling step. When applied to a data object

created the clvdata() command, the following plots can be

selected using the which option of plotting:

- Tracking plot (

which="tracking"): plots the the aggregated repeat transactions per period over a given time period. The period can be specified using theprediction.endoption. It is also possible to generate cumulative tracking plots (cumulative = FALSE). The tracking plot is the default option. - Frequency plot (

which="frequency"): plots the distribution of transactions or repeat transactions per customer, after aggregating transactions of the same customer on a single time point. The bins may be adjusted using the optiontrans.bins. (Note that iftrans.binsis changed, the option for labeling (label.remaining) usually needs to be adapted as well.) - Spending plot (

which="spending"): plots the empirical density of either customer’s average spending per transaction. Note that this includes all transactions and not only repeat-transactions. You can switch to plotting the value of every transaction for a customer (instead of the a customers mean spending) usingmean.spending=FALSE. - Interpurchase time plot (

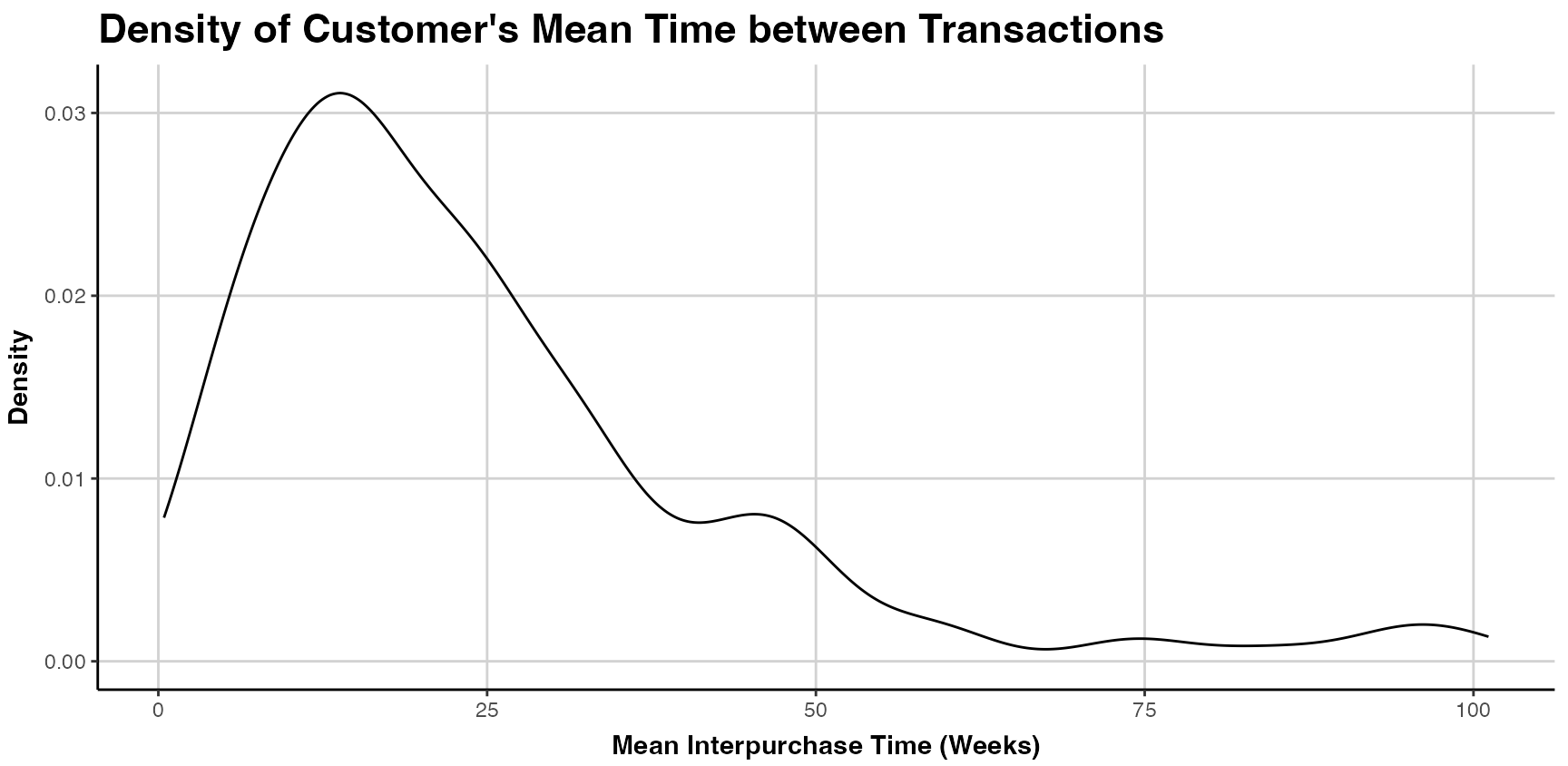

which="interpurchasetime"): plots the empirical density of customer’s mean time (in number of periods) between transactions, after aggregating transactions of the same customer on a single time point. Note that customers without repeat-transactions are note part of this plot.

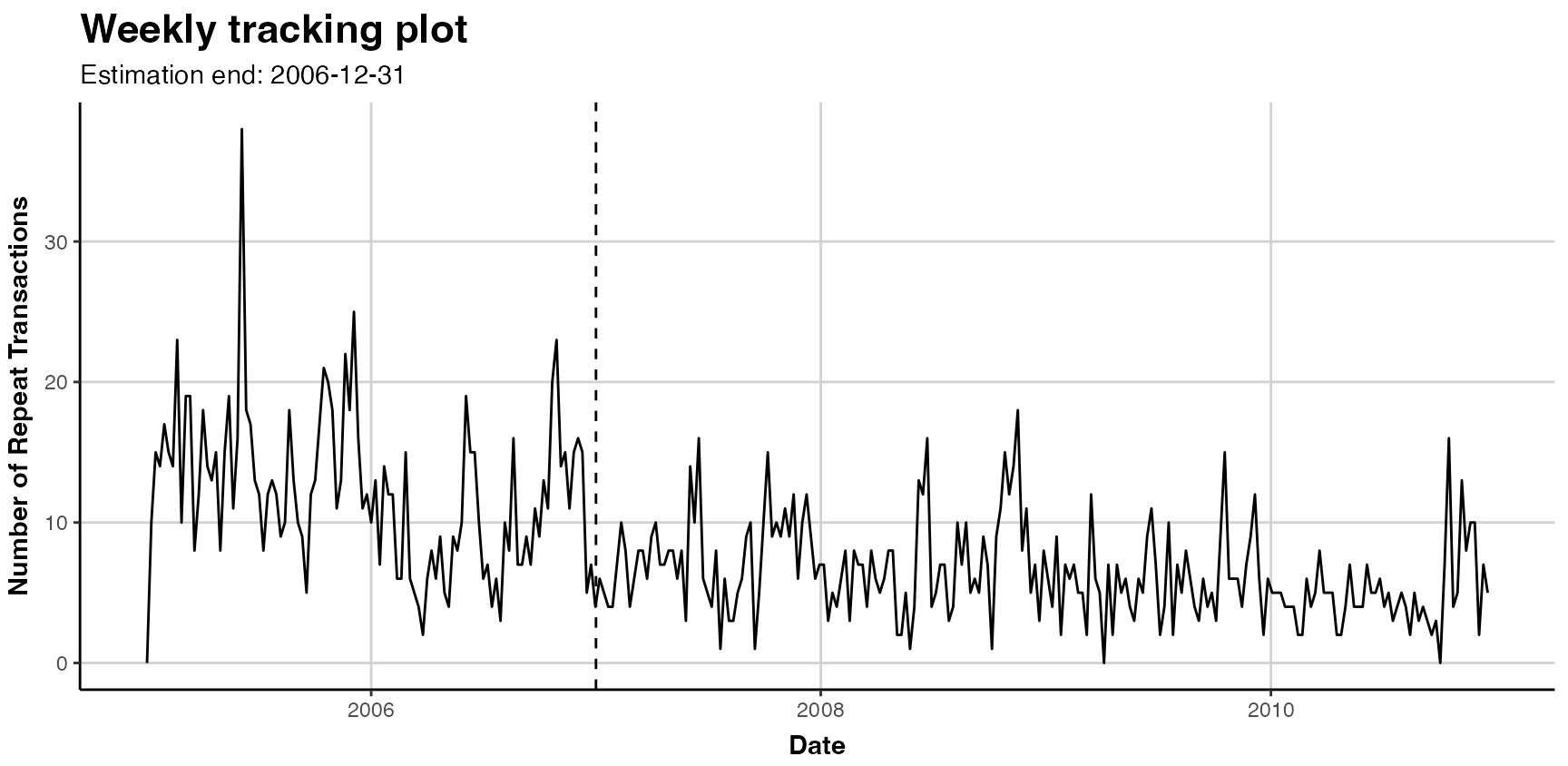

In the following, we have a basic tracking-plot for the aggregated repeat transactions

plot(clv.apparel)

#> Plotting from 2005-01-02 until 2010-12-26.

#> Warning in scale_x_date(): A <numeric> value was passed to a Date scale.

#> ℹ The value was converted to a <Date> object. To plot customers mean interpurchase time, we use:

To plot customers mean interpurchase time, we use:

plot(clv.apparel, which="interpurchasetime") When the

When the plot() command is applied to an object with the an

estimated model (i.e. est.pnbd), the following plots can be

selected using the which option of:

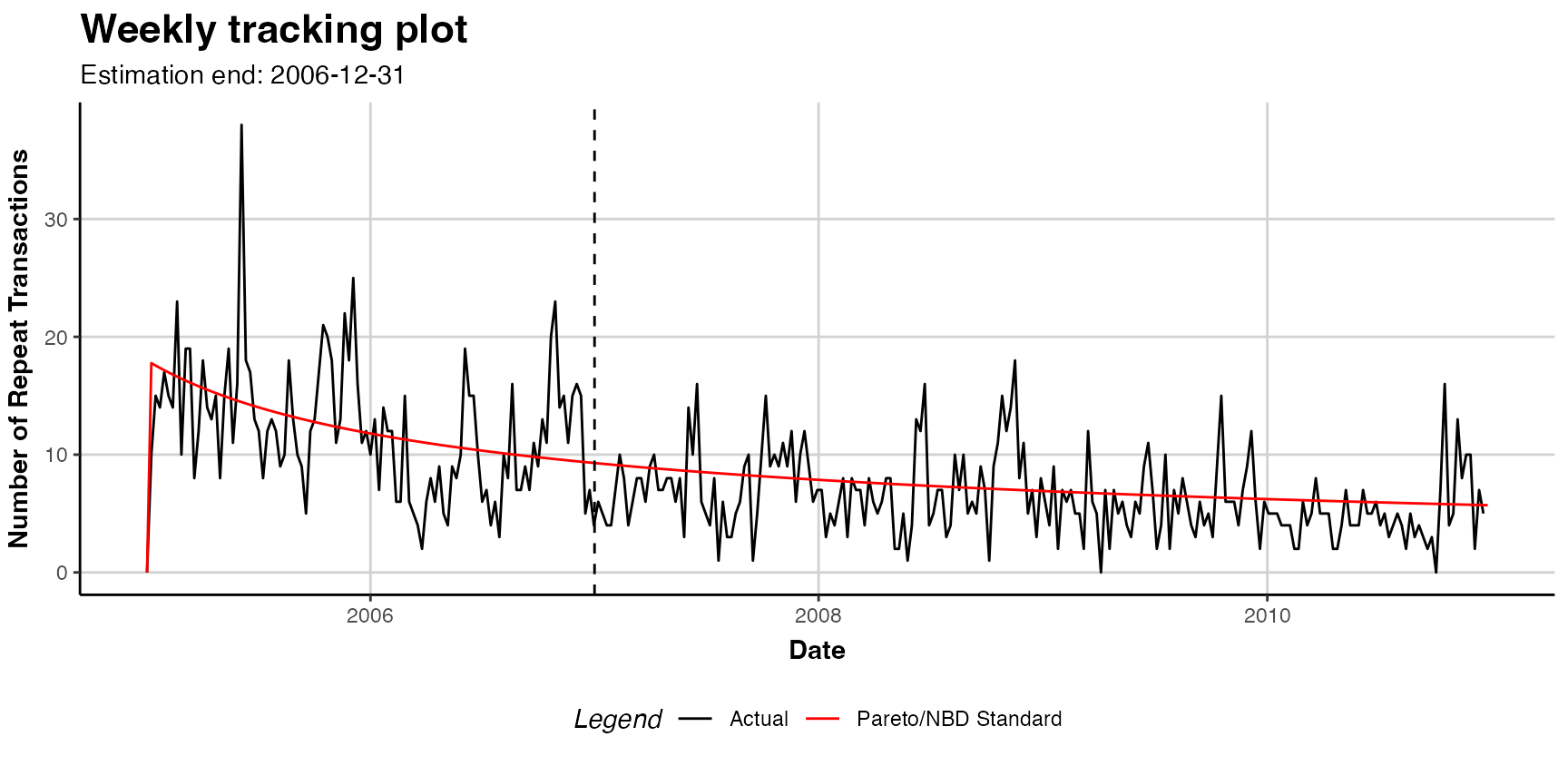

- Tracking plot (

which="tracking"): plots the actual repeat transactions and overlays it with the repeat transaction as predicted by the fitted model. Currently, following previous literature, the in-sample unconditional expectation is plotted in the holdout period. The period can be specified using theprediction.endoption. It is also possible to generate cumulative tracking plots (cumulative = FALSE). The tracking plot is th the default option. The argumenttransactionsdisable for plotting actual transactions (transactions=FALSE). For further plotting options see the documentation. Note that only whole periods can be plotted and that the prediction end might not exactly match prediction.end. See the?plot.clv.datafor more details. - Probability mass function (pmf) plot (

which="pmf"): plots the actual and expected number of customers which made a given number of repeat transaction in the estimation period. The expected number is based on the PMF of the fitted model, the probability to make exactly a given number of repeat transactions in the estimation period. For each bin, the expected number is the sum of all customers’ individual PMF value. The bins for the transactions can be adjusted using the optiontrans.bins. (Note that iftrans.binsis changed,label.remainingusually needs to be adapted as well.

For a standard tracking plot including the model, we use:

plot(est.pnbd)

#> Plotting from 2005-01-02 until 2010-12-26.

#> Warning in scale_x_date(): A <numeric> value was passed to a Date scale.

#> ℹ The value was converted to a <Date> object.

To plot the cumulative expected transactions 30 time units (30 weeks in this example) ahead of the end of the estimation plot, we use:

plot(est.pnbd, prediction.end = 30, cumulative = TRUE)Alternatively, it is possible to specify a date for the

prediction.endargument. Note that dates are rounded to the

next full time unit (i.e. week):

plot(est.pnbd, prediction.end = "2006-05-08", cumulative = TRUE)For a plot of the probability mass function (pmf), with 7 bins, we use:

plot(est.pnbd, which="pmf", trans.bins=0:5, label.remaining="6+")Covariates

CLVTools provides the option to include covariates into

probabilistic customer attrition models. Covariates may affect the

purchase or the attrition process, or both. It is also possible to

include different covariates for the two processes. However, support for

covariates is dependent on the model. Not all implemented models provide

an option for covariates. In general, CLVTools

distinguishes between two types of covariates: time-invariant and

time-varying. The former include factors that do not change over time

such as customer demographics or customer acquisition information. The

latter may change over time and include marketing activities or seasonal

patterns.

Data for time-invariant covariates must contain a unique customer ID

and a single value for each covariate. It should be supplied as a

data.frame or data.table. In the example of

the apparel retailer we use demographic information “gender” as

time-invariant and information on the acquisition channel as covariate

for both, the purchase and the attrition process. Use the

data("apparelStaticCov") command to load the time-invariant

covariates. In this example gender is coded as a dummy variable with

male=0 and female=1 and channel with

online=0 and offline=1.

data("apparelStaticCov")

apparelStaticCov

#> Id Gender Channel

#> <char> <num> <num>

#> 1: 1 0 0

#> 2: 2 1 0

#> 3: 3 1 0

#> 4: 4 1 0

#> 5: 5 1 0

#> ---

#> 596: 596 0 1

#> 597: 597 0 1

#> 598: 598 1 0

#> 599: 599 0 1

#> 600: 600 0 0Data for time-varying covariates requires a time-series of covariate

values for every customer. I.e. if the time-varying covariates are

allowed to change every week, a value for every customer for every week

is required. Note that all contextual factors are required to use the

same time intervals for the time-series. In the example of the apparel

retailer we use information on seasonal patterns

(High.Season) as time-varying covariate. Additionally, we

add gender as time-invariant contextual factors. Note that the data

structure of invariant covariates needs to be aligned with the structure

of time-varying covariate. Use data("apparelDynCov")

command to load

data("apparelDynCov")

apparelDynCov

#> Id Cov.Date High.Season Gender Channel

#> <char> <Date> <num> <num> <num>

#> 1: 1 2005-01-02 0 0 0

#> 2: 1 2005-01-09 0 0 0

#> 3: 1 2005-01-16 0 0 0

#> 4: 1 2005-01-23 0 0 0

#> 5: 1 2005-01-30 0 0 0

#> ---

#> 187796: 600 2010-11-28 1 0 0

#> 187797: 600 2010-12-05 1 0 0

#> 187798: 600 2010-12-12 0 0 0

#> 187799: 600 2010-12-19 0 0 0

#> 187800: 600 2010-12-26 0 0 0To add the covariates to an initialized clvdata object

the commands SetStaticCovariates() and

SetDynamicCovariates() are available. The two commands are

mutually exclusive. The argument clv.data specifies the

initialized object and the argument data.cov.life

respectively data.cov.trans specifies the data source for

the covariates for the attrition and the purchase process. Covariates

are added separately for the purchase and the attrition process.

Therefore if a covariate should affect both processes it has to be added

in both arguments: data.cov.life and

data.cov.trans. The arguments names.cov.life

and names.cov.trans specify the column names of the

covariates for the two processes. In our example, we use the same

covariates for both processes. Accordingly, we specify the

time-invariant covariates “Gender” and “Channel” as follows:

clv.static<- SetStaticCovariates(clv.data = clv.apparel,

data.cov.life = apparelStaticCov,

data.cov.trans = apparelStaticCov,

names.cov.life = c("Gender", "Channel"),

names.cov.trans =c("Gender", "Channel"),

name.id = "Id")To specify the time-varying contextual factors for seasonal patterns, we use the following:

clv.dyn <- SetDynamicCovariates(clv.data = clv.apparel,

data.cov.life = apparelDynCov,

data.cov.trans = apparelDynCov,

names.cov.life = c("High.Season", "Gender", "Channel"),

names.cov.trans = c("High.Season", "Gender", "Channel"),

name.id = "Id",

name.date = "Cov.Date")In order to include time-invariant covariates in a time-varying model, they may be recoded as a time-varying covariate with a constant value in every time period.

Once the covariates are added to the model the estimation process is

almost identical to the standard model without covariates. The only

difference is that the provided object now data for contains either

time-invariant or time-varying covariates and the option to define start

parameters for the covariates of both processes using the arguments

start.params.life and start.params.trans. If

not set, the staring values are set to 1. To define starting parameters

for the covariates, the name of the corresponding factor has to be used.

For example in the case of time-invariant covariates:

To execute the model estimation you have the choice between a formula-based interface and a non-formula-based interface. In the following we illustrate the two alternatives.

Estimating the model using formula interface:

We use all present covariates:

est.pnbd.static <- latentAttrition(formula = ~ .|., family = pnbd, data=clv.static)Using the formula interface, we can use only selected covariates (only Gender for the lifetime process and both, Channel and Gender for the transaction process):

est.pnbd.static <- latentAttrition(formula = ~ Gender|Channel+Gender,

family = pnbd, data=clv.static)Or we can transform covariates:

est.pnbd.static <- latentAttrition(formula = ~ Channel+Gender|I(log(Channel+2)),

family = pnbd, data=clv.static)Analogously, we can estimate the model containing time-varying covariates. In this example we also activate output of the optimizer in order to observe the progress.

est.pnbd.dyn <- latentAttrition(formula = ~ .|., family = pnbd, data = clv.dyn,

optimx.args = list(control=list(trace=5)))Estimating the model using non-formula interface:

est.pnbd.static <- pnbd(clv.static,

start.params.model = c(r=1, alpha = 2, s = 1, beta = 2),

start.params.life = c(Gender=0.6, Channel=0.4),

start.params.trans = c(Gender=0.6, Channel=0.4))

#> Starting estimation...

#> Estimation finished!It is not possible to alter or select covariates in the non-formula interface, but, we can also estimate a model containing time-varying covariates:

est.pnbd.dyn <- pnbd(clv.dyn,

start.params.model = c(r=1, alpha = 2, s = 1, beta = 2),

start.params.life = c(High.Season=0.5, Gender=0.6, Channel=0.4),

start.params.trans = c(High.Season=0.5, Gender=0.6, Channel=0.4),

optimx.args = list(control=list(trace=5)))To inspect the estimated model we use summary(), however

all other commands such as print(), coef(),

loglike(), confint() and vcov()

are also available. Now, output contains also parameters for the

covariates for both processes. Since covariates are added separately for

the purchase and the attrition process, there are also separate model

parameters for the two processes. Note that while significance

indicators are NA for the main model parameters, they are

present for the covariate parameters because a hypothesis test relative

to a null of 0 does make sense for them. These parameters are directly

interpretable as rate elasticity of the corresponding factors: A 1%

change in a contextual factor $\bf{X}^{P}$ or $\bf{X}^{L}$ changes the purchase or the

attrition rate by $\gamma_{purch}\bf{X}^{P}$ or $\gamma_{life}\bf{X}^{L}$ percent,

respectively (Gupta 1991). In the example

of the apparel retailer, we observe that female customer purchase

significantly more (trans.Gender=1.42576). Note, that

female customers are coded as 1, male customers as 0. Also customers

acquired offline (coded as Channel=1), purchase more

(trans.Channel=0.40304) and stay longer

(life.Channel=0.9343). Make sure to check the

Karush-Kuhn-Tucker optimality conditions of the first and second order

(Kuhn and Tucker 1951) (KKT1 and KKT1)

before interpreting the parameters. If those criteria are not met, the

optimizer has probably not arrived at an optimal solution. If this is

the case it is usually a good idea to rerun the estimation using

alternative starting values.

summary(est.pnbd.static)

#> Pareto/NBD with Static Covariates Model

#>

#> Call:

#> pnbd(clv.data = clv.static, start.params.model = c(r = 1, alpha = 2,

#> s = 1, beta = 2), start.params.life = c(Gender = 0.6, Channel = 0.4),

#> start.params.trans = c(Gender = 0.6, Channel = 0.4))

#>

#> Fitting period:

#> Estimation start 2005-01-02

#> Estimation end 2006-12-31

#> Estimation length 104.0000 Weeks

#>

#> Coefficients:

#> Estimate Std. Error z-val Pr(>|z|)

#> r 1.8387 0.3457 NA NA

#> alpha 92.9435 16.9749 NA NA

#> s 0.5913 0.2603 NA NA

#> beta 49.5048 36.1444 NA NA

#> life.Gender -0.6428 0.2956 -2.175 0.02965 *

#> life.Channel 0.7902 0.3058 2.584 0.00978 **

#> trans.Gender 0.2860 0.1041 2.746 0.00603 **

#> trans.Channel 0.6239 0.1049 5.945 2.76e-09 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Optimization info:

#> LL -5821.0627

#> AIC 11658.1254

#> BIC 11693.3008

#> KKT 1 TRUE

#> KKT 2 TRUE

#> fevals 60.0000

#> Method L-BFGS-B

#>

#> Used Options:

#> Correlation FALSE

#> Regularization FALSE

#> Constraint covs FALSETo predict future customer behavior we use predict().

Note that dependent on the model, the predicted metrics may differ. For

example, in the case of the Pareto/NBD model with time-varying

covariates, instead of DERT, DECT is predicted. DECT only covers a

finite time horizon in contrast to DERT. Time-varying covariates must be

provided for the entire prediction period. If the data initially

provided in the SetDynamicCovariates() command does not

cover the complete prediction period, the argument new.data

offers the ability to supply new data for the time-varying covariates in

the from of a clvdata object.

Add Correlation to the model

To relax the assumption of independence between the purchase and the

attrition process, CLVTools provides the option to specify

the argument use.cor when fitting the model

(i.e. pnbd). In case of use.cor=TRUE, a

Sarmanov approach is used to correlate the two processes.

start.param.cor allows to optionally specify a starting

value for the correlation parameter. Correlation can be added with or

without covariates.

To execute the model estimation you have the choice between a formula-based interface and a non-formula-based interface. In the following we illustrate the two alternatives.

Estimating the model using formula interface:

est.pnbd.cor <- latentAttrition(formula = , family = pnbd,

use.cor=TRUE, data=clv.apparel)Estimating the model using non-formula interface:

The parameter Cor(life,trans) is added to the parameter

estimates that may be directly interpreted as a correlation. In the

example of the apparel retailer the correlation parameter is not

significant and the correlation is very close to zero, indicating that

the purchase and the attrition process may be independent.

Advanced Options for Covariates

CLVTools provides two additional estimation options for

models containing covariates (time-invariant or time-varying):

regularization and constraints for the parameters of the covariates.

Support for this option is dependent on the model. They may be used

simultaneously.

In the following we illustrate code for both, a formula-based interface a non-formula-based interface.

Regularization helps to prevent overfitting

of the model when using covariates. We can add regularization lambdas

for the two processes. The larger the lambdas the stronger the effects

of the regularization. Regularization only affects the parameters of the

covariates. The use of regularization is indicated at the end of the

summary() output.

Estimating the model using formula interface:

est.pnbd.reg <- latentAttrition(formula = ~ .|., family = pnbd,

reg.lambdas=c(life=3, trans=8), data=clv.static)

summary(est.pnbd.reg)Estimating the model using non-formula interface:

We use the argument reg.lambdas to specify the lambdas

for the two processes

(i.e. reg.lambdas = c(trans=100, life=100):

est.pnbd.reg <- pnbd(clv.static,

start.params.model = c(r=1, alpha = 2, s = 1, beta = 2),

reg.lambdas = c(trans=100, life=100))

summary(est.pnbd.reg)Constraints implement equality constraints

for contextual factors with regards to the two processes. For example

the variable “gender” is forced to have the same effect on the purchase

as well as on the attrition process. We can use the argument

names.cov.constr(i.e. names.cov.constr=c("Gender")).

In this case, the output only contains one parameter for “Gender” as it

is constrained to be the same for both processes. To provide starting

parameters for the constrained variable use

start.params.constr. The use of constraints is indicated at

the end of the summary() output.

Estimating the model using formula interface:

est.pnbd.constr <- latentAttrition(formula = ~.|., family = pnbd, data = clv.static,

names.cov.constr=c("Gender"),

start.params.constr = c(Gender = 0.6))

summary(est.pnbd.constr)Note: providing a starting parameter for the constrained variable is optional.

Customer Spending

Customer lifetime value (CLV) is composed of three components of

every customer: the future level of transactions, expected attrition

behaviour (i.e. probability of being alive) and the monetary value.

While probabilistic latent attrition models provide metrics for the

first two components, they do not predict customer spending. To predict

customer spending an additional model is required. The

CLVToolspackage features the Gamma/Gamma (G/G) (Fader, Hardie, and Lee 2005b; Colombo and Jiang

1999) model for predicting customer spending. For convenience,

the predict() command allows to automatically predict

customer spending for all latent attrition models using the option

predict.spending=TRUE (see section Customer Spending). However, to provide more

options and more granular insights the Gamma/Gamma model can be

estimated independently. In the following, we discuss how to estimate a

Gamma/Gamma model using CLVTools.

The general workflow remains identical. It consists of the three main

steps: (1) creating a clv.data object containing the

dataset and required meta-information, (2) fitting the model on the

provided data and (3) predicting future customer purchase behavior based

on the fitted model.

CLVTools provides two ways for evaluating spending

models: you can use of the formula interface or you can use standard

functions (non-formula interface). Both offer the same functionality.

Through out this walkthrough, we will illustrate both options.

Reporting and plotting results is facilitated by the implementation

of well-known generic methods such as plot(),

print() and summary().

Load sample data provided in the package

For estimating customer spending CLVTools requires

customers’ transaction history including price. Every transaction record

consists of a purchase date,customer ID and the price of the

transaction. Data may be provided as data.frame or

data.table (Dowle and Srinivasan

2019). Currently, the Gamma/Gamma model does not allow for

covariates.

We use again simulated data comparable to data from a retailer in the

apparel industry. The apparel dataset is available in the

CLVTools package. We use the

data(apparelTrans) to load it and initialize a data object

using the clvdata() command. For details see section Initialize the CLV-Object.

data("apparelTrans")

apparelTrans

#> Id Date Price

#> <char> <Date> <num>

#> 1: 1 2005-01-02 230.30

#> 2: 1 2005-09-06 84.39

#> 3: 1 2006-01-18 131.07

#> 4: 1 2006-04-05 86.43

#> 5: 1 2006-07-02 11.49

#> ---

#> 3183: 600 2005-01-02 24.94

#> 3184: 600 2005-04-17 54.97

#> 3185: 600 2005-06-30 66.84

#> 3186: 600 2005-10-27 22.54

#> 3187: 600 2006-01-09 12.97

clv.apparel <- clvdata(apparelTrans,

date.format="ymd",

time.unit = "week",

estimation.split = 40,

name.id = "Id",

name.date = "Date",

name.price = "Price")Estimate Model Parameters

To estimate the Gamma/Gamma spending model, we use the command

gg() on the initialized clvdata object.

clv.data specifies the initialized object prepared in the

last step. Optionally, starting values for the model parameters and

control settings for the optimization algorithm may be provided: The

argument start.params.model allows to assign a vector of

starting values for the optimization (i.e

c(p=1, q=2, gamma=1) for the the Gamma/Gamma model). This

is useful if prior knowledge on the parameters of the distributions are

available. By default starting values are set to 1 for all parameters.

The argument optimx.args provides an option to control

settings for the optimization routine (see section Estimate Model Parameters).

In line with literature, CLVTools does not use by

default the monetary value of the first transaction to fit the model

since it might be atypical of future purchases. If the first transaction

should be considered the argument remove.first.transaction

can be set to FALSE.

To execute the model estimation you have the choice between a formula-based interface and a non-formula-based interface. In the following we illustrate the two alternatives.

Estimating the model using formula interface:

est.gg <- spending(family = gg, data=clv.apparel)

#> Starting estimation...

#> Estimation finished!

est.gg

#> Gamma-Gamma Model

#>

#> Call:

#> spending(family = gg, data = clv.apparel)

#>

#> Coefficients:

#> p q gamma

#> 3.675 4.630 36.111

#> KKT1: TRUE

#> KKT2: TRUEUsing start parameters or other additional arguments for the optimizer:

est.gg <- spending(family = gg, data=clv.apparel,

optimx.args = list(control=list(trace=5)),

start.params.model=c(p=0.5, q=15, gamma=2))Specify the option to NOT remove the first transaction:

est.gg <- spending(family = gg, data=clv.apparel,

remove.first.transaction=FALSE)Predict Customer Spending

Once the model parameters are estimated, we are able to predict

future customer mean spending on an individual level. To do so, we use

predict() on the object with the estimated parameters

(i.e. est.gg). Note that there is no need to specify a

prediction period as we predict mean spending.

In general, probabilistic spending models predict the following expected characteristic for every customer:

- predicted mean spending (“predicted.mean.spending”)

If a holdout period is available additionally the true mean spending (“actual.mean.spending”) during the holdout period is reported.

To use the parameter estimates on new data (e.g., an other customer

cohort), the argument newdata optionally allows to provide

a new clvdata object.

results.spending <- predict(est.gg)

print(results.spending)

#> Key: <Id>

#> Id actual.mean.spending predicted.mean.spending

#> <char> <num> <num>

#> 1: 1 104.82000 60.62446

#> 2: 10 31.65500 37.71808

#> 3: 100 37.03889 36.56190

#> 4: 101 0.00000 33.24045

#> 5: 102 0.00000 36.56190

#> ---

#> 596: 95 22.76000 28.96908

#> 597: 96 84.53667 36.56190

#> 598: 97 0.00000 36.56190

#> 599: 98 33.14000 36.56190

#> 600: 99 13.99000 17.43526Plot Spendings

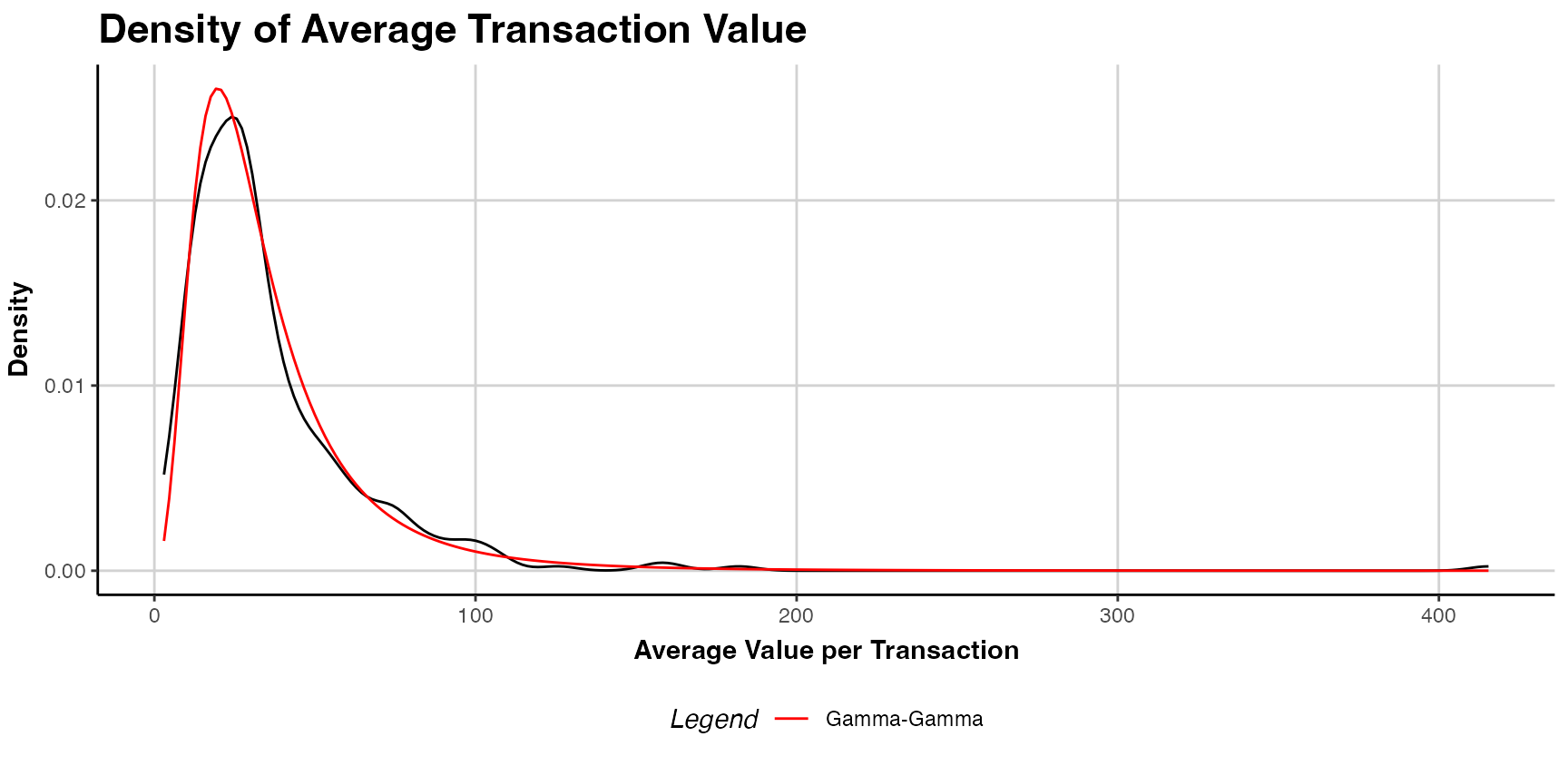

an estimated spending model object (i.e. est.gg) may be

plotted using the plot() command. The plot provides a

comparison of the estimated and actual density of customer spending. The

argument plot.interpolation.points allows to adjust the

number of interpolation points in density graph.

plot(est.gg)